Directors first appointed during the tax year have a pro rata annual earnings period for the remainder of that tax year for the calculation of NIC.

The number of weeks in the pro rata annual earnings period is

- the tax week of appointment, and

- the remaining tax weeks in the tax year

Please note: there are 53 weeks in the tax year but only 52 weeks are used when working out the pro rata period. If someone is appointed in week 53, the pro rata period is 1 week.

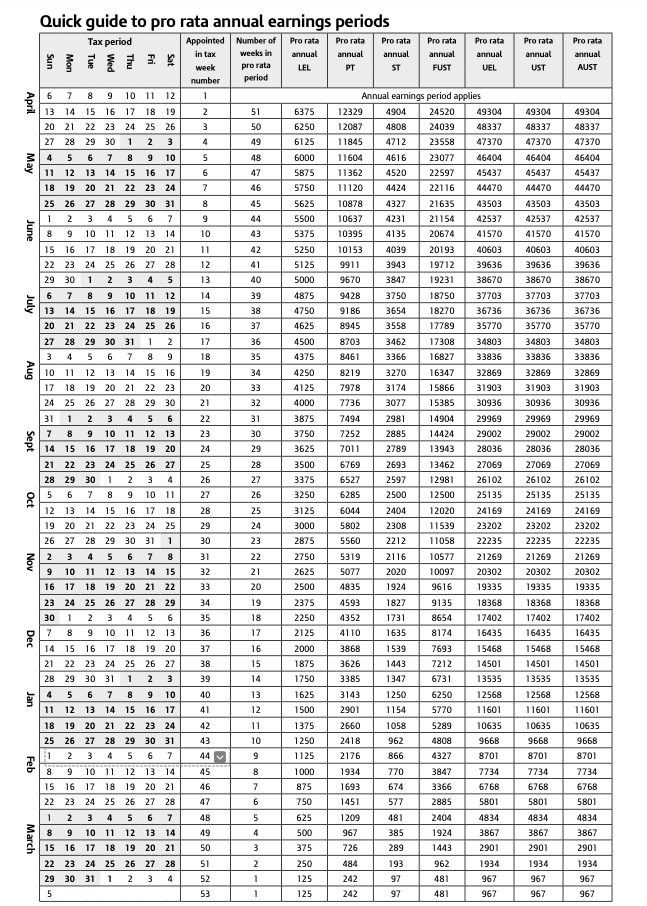

Example

A director is appointed in tax week 30.

The number of weeks in the pro rata annual earnings period is 23 weeks and the director will therefore have the following pro rata annual NI thresholds:

- Pro rata annual LEL: £2,875

- Pro rata annual PT: £5,560

- Pro rata annual ST: £2,212

- Pro rata annual UEL: £22,235

Quick Guide to the Pro Rata Annual Earnings Periods for 2025-26

Please note: if someone is appointed in week 53, the pro rata period is 1 week.

FAQs - Directors apppointed in the year

Q. We’ve added a director as a new starter in this tax year, but they’ve actually been a director all year. BrightPay is calculating employee NIC, but there shouldn’t be any. Why?

A. BrightPay is using the employment start date you entered, which overrides the directorship start date and prevents the full annual NIC threshold being used for the director.

If they have been a director for the whole tax year and simply weren’t paid until later in the tax year, remove the employment start date so only the directorship start date applies. BrightPay will then calculate NIC on the full annual basis.

Depending on how your payroll is set up, you may also need to finalise the earlier periods in the year with zero pay to reach period you wish to pay.